Interesting Insider Buys [2023-04-25]

Some Insider Buying That Makes You Go… Hmm 🤔

We monitor every purchase or sale of stock by insiders, every day. If we see management purchasing millions of dollars of their own stock in the public markets, it doesn't necessarily mean that it's a good investment, but it does mean that we should print out the proxy and annual report to determine if we too think it might be an attractive investment.

We study total stock ownership by management, how that ownership was accumulated, and most critically, we seek to understand total stock ownership as it relates to compensation. Simply, we seek to invest with management teams that have more to gain or lose through their equity ownership than they do through their compensation.

A habit that I’ve picked up over the years is scanning the insider buying / selling lists everyday (OpenInsider and Dataroma are great free websites). Of course, not all insider buying or selling is interesting, but sometimes it pays off (and sometimes it doesn’t). Some examples:

Worked: Back in 2019, Old West noticed that the new CEO of Bunge BG 0.00%↑ bought ~$9m of stock in the $40-$54 range; currently it’s trading around ~$90 (and even hit ~$124 back in April 2022)

Didn’t Work: B. Riley Financial RILY 0.00%↑ is a case where insiders have been consistently buying since 2020 (and even earlier I believe) - from $20 all the way to $78 and back down to $30. The stock currently sits ~$30. I’ve publicly tweeted about the sheer amount of buying - unfortunately, those who followed insiders into the stock haven’t had much to write home about (yet?)

There’s clearly an art to deciphering insider transactions.

Anyways - below are a few interesting situations of insider buying that I’ve been looking at and hopefully will be of interest to you.

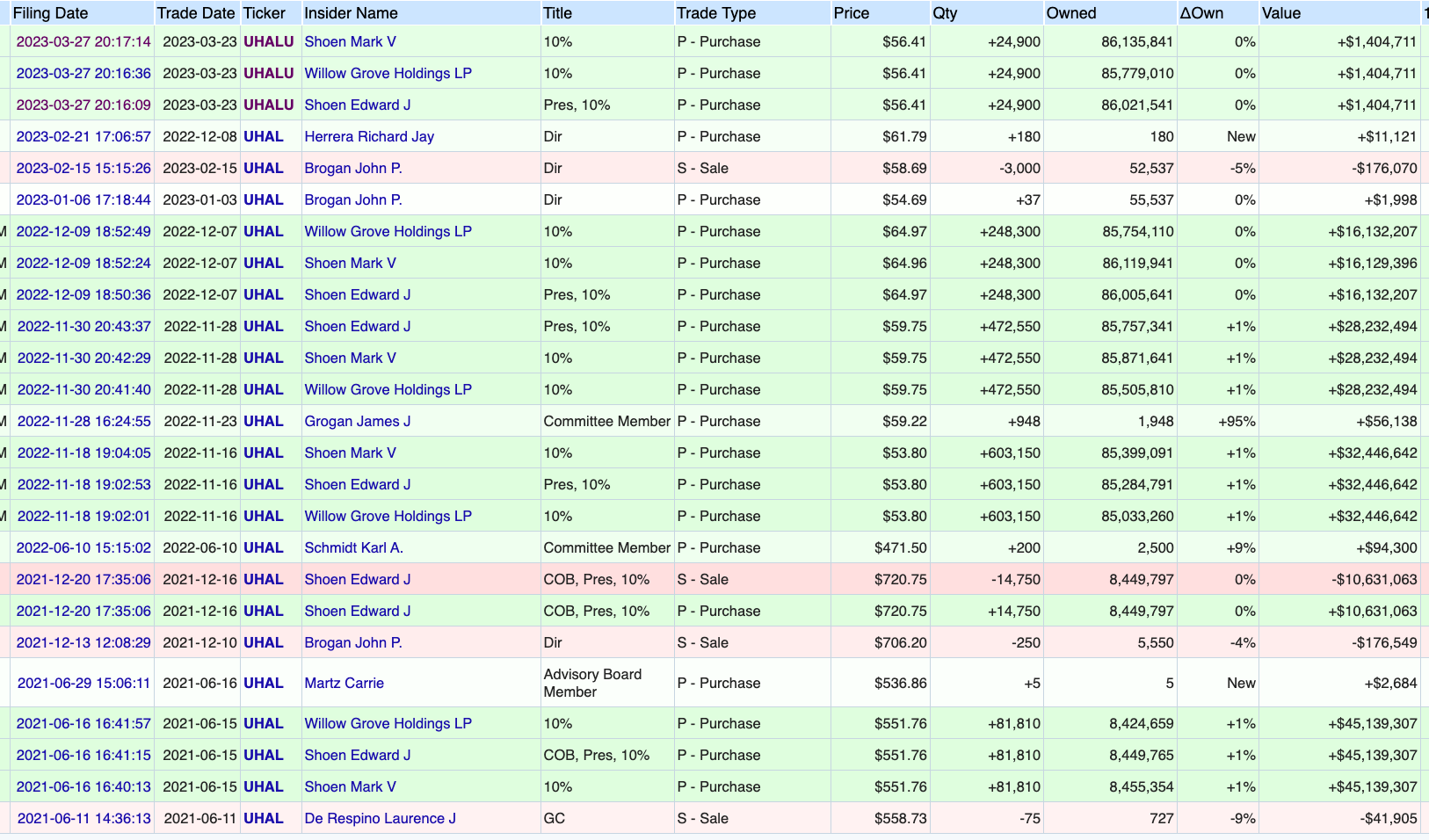

(1) U-Haul Holding Co UHAL 0.00%↑

North America’s largest “do-it-yourself” moving and storage operator through our subsidiary U- Haul International, Inc. (“U-Haul”); synonymous with “do-it-yourself” (10.50B market cap)

Trades at 11.1x PE, 2.1x EV/S, 5.5x EV/EBITDA

History of growing sales, earnings, and FCF

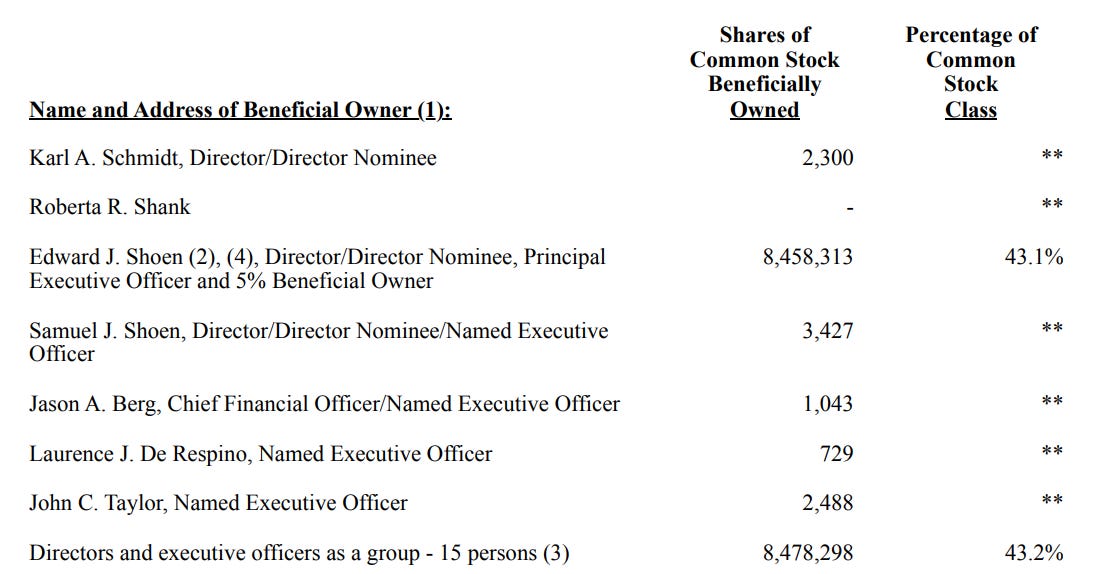

Insiders own ~43% of the company

1 analyst coverage

From a VIC write-up from August 2022:

The business is stronger than ever and the market overestimates UHAL’s COVID benefit.

UHAL’s brand equity and related competitive moat is underappreciated.

The stock is cheaper and the business more overcapitalized than ever.

Management talks openly about taking actions to close the long persisting valuation gap.

(2) Ryan Specialty Group Holdings RYAN 0.00%↑

Operates as a service provider of specialty products and solutions for insurance brokers, agents, and carriers; offers distribution, underwriting, product development, administration, and risk management services by acting as a wholesale broker and a managing underwriter ($10.48B market cap)

Which of course, sent me down a rabbit hole of figuring out what “wholesale brokerage businesses” were. Here’s a great post by Chris Mayer (author of 100-Baggers) on Brown & Brown and insurance brokers:

The Greatest Industry in the History of Mankind?

“The good news is that irrespective of value, we believe there will continue to be a healthy demand for insurance agencies given high recurring revenue, low capital expenditure requirements, strong EBITDA margins and fairly high barriers to entry. In my opinion, even with a correction, the insurance distribution system will remain the greatest industry in the history of mankind.” -John Wepler, Chairman of MarshBerry

Recently, the U.S. government blocked a merger between Aon and Willis Tower. The particulars don’t interest me, but I read through the legal briefs and was struck by the discussion of the competitive advantages of these firms.

To wit, the government used the CEO’s own words against him. Citing Willis Towers’ annual report in 2018 where he wrote “[h]igh barriers to entry, existing market share, brand recognition and long-term client relationships give incumbents the edge over newcomers.”

And further, the government noted “the prevalence of post-employment non-compete and non-solicit clauses in the insurance broking industry, including by Aon and WTW, serve as barriers to attracting clients away from the Big Three [Aon, Marsh and Willis Tower].”

Finally, and my favorite part, the government cited the failure of competitors to break through those barriers:

“Past attempts have shown that successful entry is difficult. For example, several years ago a number of employees from one of the Big Three attempted to start their own commercial risk broking firm with a focus on serving large customers.

“Despite having deep experience in the industry and existing relationships with many potential customers, this new venture failed to take much business from Aon, WTW, and Marsh.

In short, insurance brokers are fantastic businesses and fall under the tollbooth or croupier business model. Of course, being a newcomer, RYAN has some challenges (started in 2010) but the CEO seems confident…

"In practice, insurance brokers have many of the characteristics of exchanges. They do not generally risk their own capital, and they earn a fee for the facilitation of the transactions of others." - Murray Stahl

The CEO / founder owns 13.4% (72% of the votes) and management owns 15.2% (80% of the votes)

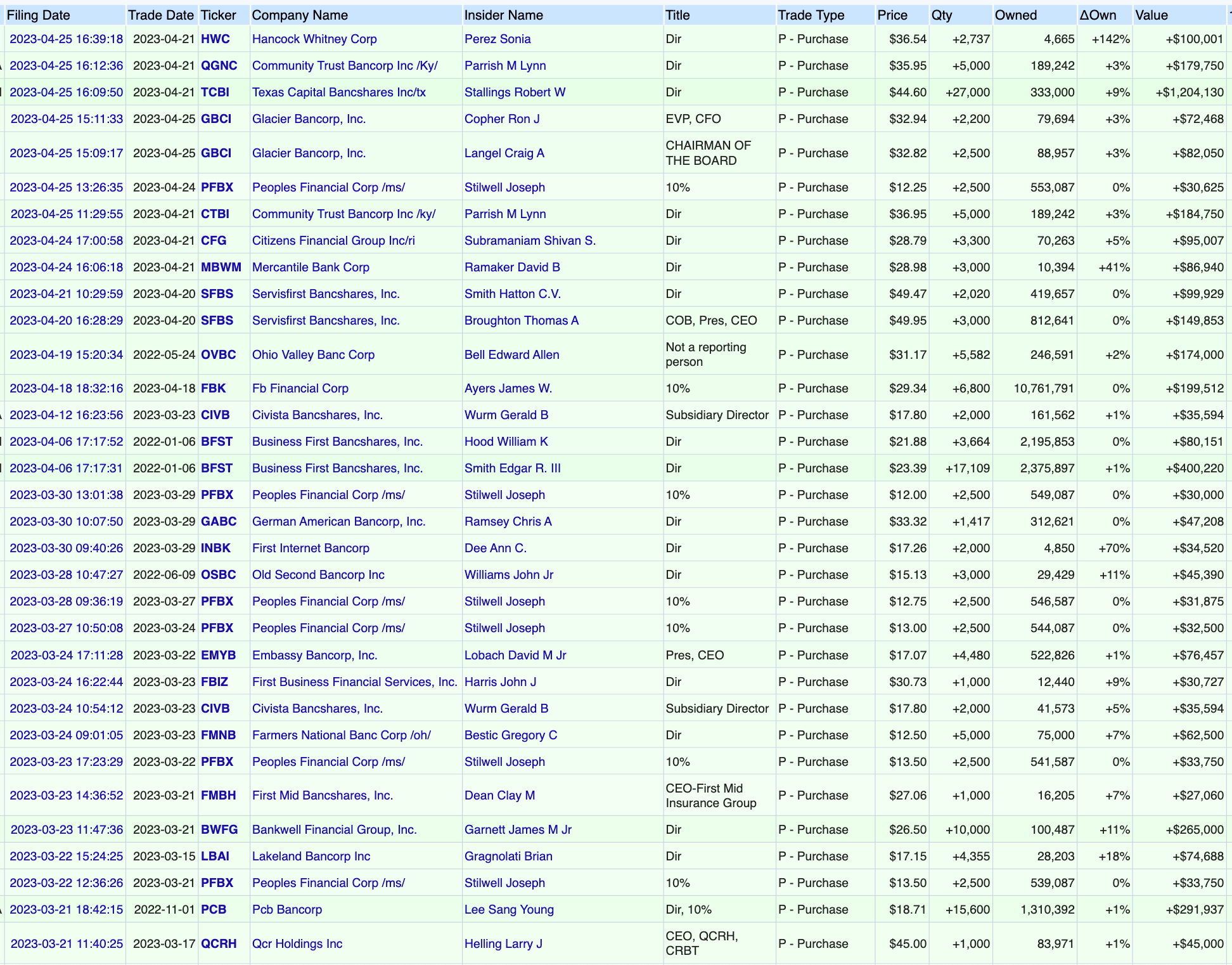

(3) Regional Banks

Insider buying across sectors / industries provide an interesting viewpoint. The Silicon Valley Bank / Signature Bank collapses in early March sent investors scrambling from US Regional Banks (a quick look at IAT - iShares U.S. Regional Banks ETF - shows it’s down ~33% since the debacle)

Yet the list below shows that insiders at certain regional banks are stepping in to buy shares.

OpenInsider: State Commercial Banks

I think this could actually be a REALLY great idea for a dedicated substack or release schedule.

The RC is must read weekend time.